Are Big Investors Really Buying Up All the Homes? Here’s the Truth.

It’s hard to scroll online lately without seeing some version of this claim: “Big investors are buying up all the homes.” And honestly, if you’re a homebuyer who’s lost out on a few offers, that idea probably sounds believable. When homes are expensive and competition is tight, it’s easy to assume g

Read More

Is the Housing Market Going To Crash? Here’s What Experts Say

If you’ve seen headlines or social posts calling for a housing crash, it’s easy to wonder if home values are about to take a hit. But here’s the simple truth. The data doesn’t point to a crash. It points to slow, continued growth. And sure, it’s going to vary by local area. Some markets will see pri

Read More

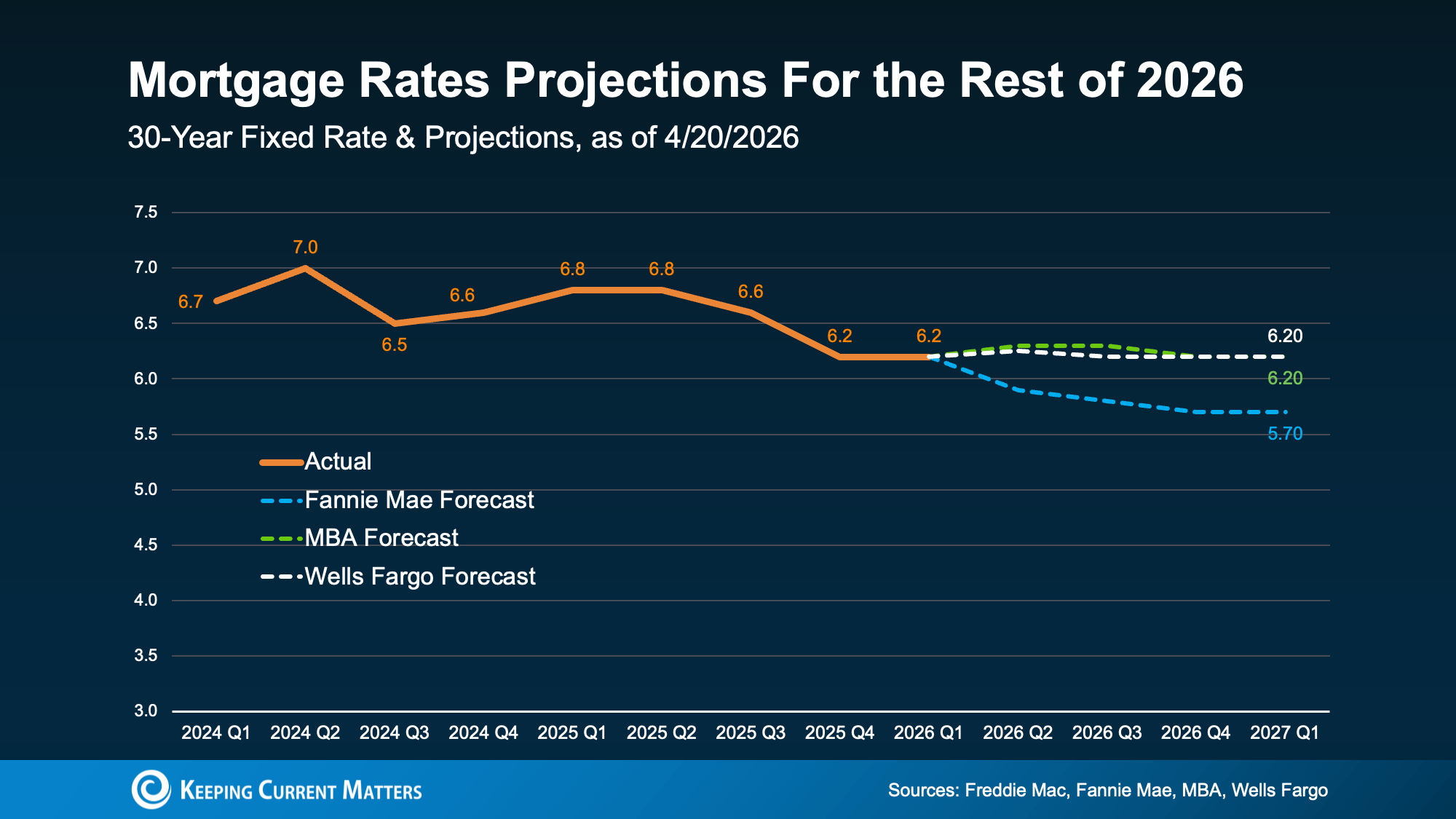

2026 Housing Market Outlook

After a couple of years where the housing market felt stuck in neutral, 2026 may be the year things shift back into gear. Expert forecasts show more people are expected to move – and that could open the door for you to do the same. More Homes Will Sell With all of the affordability challenges at pla

Read More

Housing Market Forecasts for the Rest of 2025

If you’ve been watching the market, you’ve likely noticed a few changes already this year. But what’s next? From home prices to mortgage rates, here’s what the latest expert forecasts suggest for the rest of 2025 – and what these shifts could mean for you. Will Home Prices Fall? We' know many buyers

Read More

Categories

- All Blogs (251)

- Affordability (18)

- Agent Value (6)

- Buying & Selling (116)

- Buying Tips (47)

- Downsize (2)

- Economy (1)

- Equity (3)

- First Time Home Buyers (58)

- For Buyers (22)

- For Sale By Owner (8)

- for sellers (13)

- Forecast (5)

- Home Buyers (159)

- Home Owner (24)

- Home Owners (23)

- Home Prices (17)

- Housing Market (109)

- Inventory (11)

- Mortgage Rates (50)

- Move-Up (2)

- New Construction (9)

- Real Estate (154)

- Real Estate Investing (4)

- Rent vs. Buy (2)

- Selling Tips (28)

- Selling Your Home (95)

- Senior Market (1)

Recent Posts