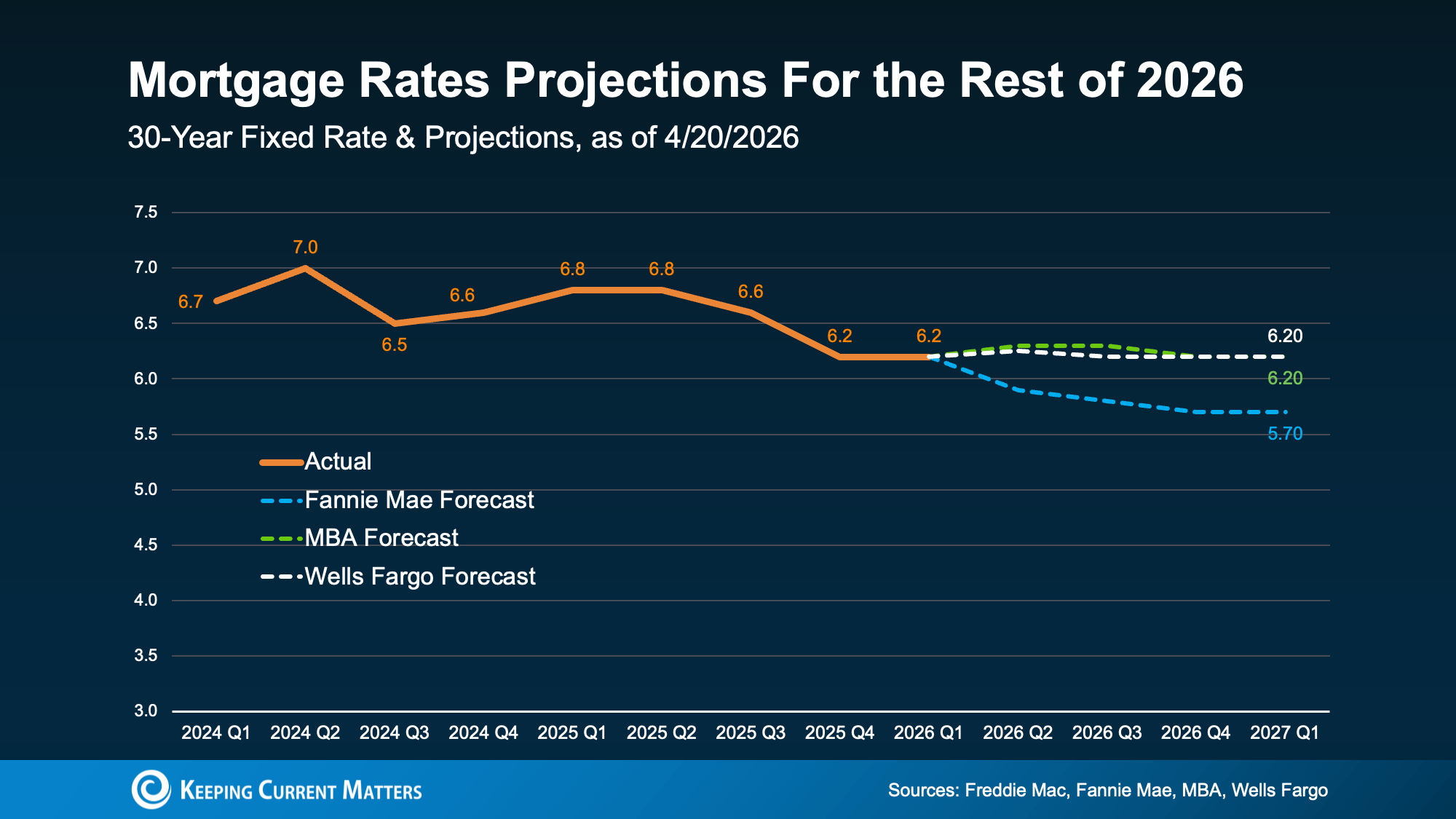

You Can’t Control What’s Happening with Mortgage Rates. But You Can Control This.

Mortgage rates have been volatile lately. And if you’re thinking about buying a home, that can make it harder to plan. But there are still things you can do to get the best rate possible in today’s market. It starts with having the right information. So, what’s causing the bumps in rates? And what c

Read More

Wondering If You Should Still Buy a Home Right Now? Here’s What To Keep in Mind.

With economic headlines, global events, and near constant talk about affordability, you may be wondering if this is the right time to move. But here’s what you need to remember. While recent events do have some impact on the housing market, they don’t take buying off the table. You just have to use

Read More

3 Things That Are Not Going To Happen in Today's Housing Market

There’s a lot of uncertainty right now and that’s leading to some dramatic headlines. And if you’re thinking about buying a home, that can make you feel a little less sure about your decision. A recent study by CNBC asked homebuyers what they’re most worried about, and three themes kept coming up ag

Read More

Mortgage Rates Recently Hit a 3-Year Low. Here’s Why That’s Still a Big Deal.

If you’re one of the thousands of homebuyers waiting for rates to fall, you should know it’s already happening. And they recently crossed an important milestone. Rates officially dipped their toes into the 5s – something that hasn’t happened in about 3 years. This moment marked a critical threshold.

Read More

Categories

- All Blogs (262)

- Affordability (20)

- Agent Value (9)

- Buying & Selling (117)

- Buying Tips (51)

- Downsize (3)

- Economy (1)

- Equity (5)

- First Time Home Buyers (61)

- For Buyers (26)

- For Sale By Owner (9)

- for sellers (20)

- Forecast (5)

- Home Buyers (161)

- Home Owner (27)

- Home Owners (26)

- Home Prices (20)

- Housing Market (109)

- Inventory (11)

- Mortgage Rates (50)

- Move-Up (2)

- New Construction (9)

- Price It Right/Overpricing (1)

- Real Estate (154)

- Real Estate Investing (4)

- Rent vs. Buy (2)

- Selling Tips (33)

- Selling Your Home (98)

- Senior Market (2)

Recent Posts