The Secret To Selling Your House in Today’s Market

A few years ago, homes were flying off the shelves and getting multiple offers well over their asking price. It felt like you could name your price and still have buyers lined up at the door. But today’s housing market is different. Buyers are getting more selective now that inventory has grown. Hom

Read More

Real Estate Is Voted the Best Long-Term Investment 12 Years in a Row

Some Highlights In a recent poll from Gallup, real estate has once again been voted the best long-term investment. And it’s claimed that top spot for 12 straight years now. That’s because homeownership is one of the top ways to build your wealth, even with home price growth moderating and ongoing ec

Read More

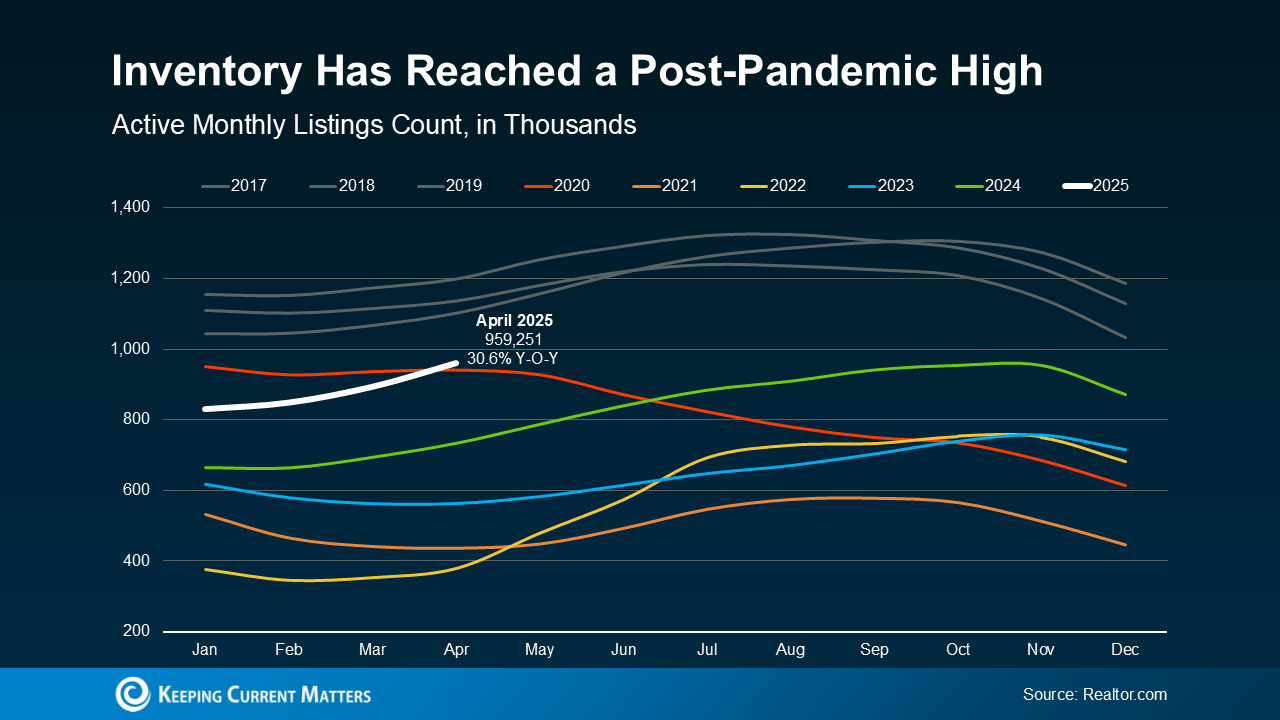

More Homes for Sale Isn’t a Warning Sign – It's Your Buying Opportunity

Maybe you’ve heard the number of homes for sale has reached a recent high. And it might make you question if this is the start of another housing market crash. But the reality is, the data proves that’s just not the case. In most areas, more inventory isn’t bad news. It’s actually a sign of the mark

Read More

Housing Market Forecasts for the Second Half of the Year

From rising home prices to mortgage rate swings, the housing market has left a lot of people wondering what’s next – and whether now is really the right time to move. There is one place you can turn to for answers you want the most. And that’s the experts. Leading housing experts are starting to rel

Read More

Categories

- All Blogs (263)

- Affordability (21)

- Agent Value (9)

- Buying & Selling (117)

- Buying Tips (52)

- Downsize (3)

- Economy (1)

- Equity (5)

- First Time Home Buyers (62)

- For Buyers (27)

- For Sale By Owner (9)

- for sellers (20)

- Forecast (5)

- Home Buyers (162)

- Home Owner (27)

- Home Owners (26)

- Home Prices (20)

- Housing Market (109)

- Inventory (11)

- Mortgage Rates (50)

- Move-Up (2)

- New Construction (10)

- Price It Right/Overpricing (1)

- Real Estate (154)

- Real Estate Investing (4)

- Rent vs. Buy (2)

- Selling Tips (33)

- Selling Your Home (98)

- Senior Market (2)

Recent Posts